Page 139 - Martin Marietta - 2023 Proxy Statement

P. 139

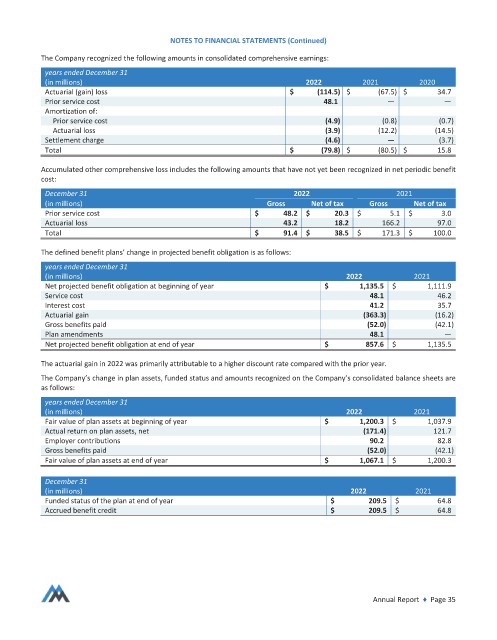

NOTES TO FINANCIAL STATEMENTS (Continued)

The Company recognized the following amounts in consolidated comprehensive earnings:

years ended December 31

(in millions) 2022 2021 2020

Actuarial (gain) loss $ (114.5) $ (67.5) $ 34.7

Prior service cost 48.1 — —

Amortization of:

rior service cost (4.9) (0.8) (0.7)

Actuarial loss (3.9) (12.2) (14.5)

Settlement charge (4.6) — (3.7)

Total $ (79.8) $ (80.5) $ 15.8

Accumulated other comprehensive loss includes the following amounts that have not yet been recognized in net periodic benefit

cost:

December 31 2022 2021

(in millions) Gross Net of tax Gross Net of tax

rior service cost $ 48.2 $ 20.3 $ 5.1 $ 3.0

Actuarial loss 43.2 18.2 166.2 97.0

Total $ 91.4 $ 38.5 $ 171.3 $ 100.0

The defined benefit plans’ change in projected benefit obligation is as follows:

years ended December 31

(in millions) 2022 2021

Net projected benefit obligation at beginning of year $ 1,135.5 $ 1,111.9

Service cost 48.1 46.2

Interest cost 41.2 35.7

Actuarial gain (363.3) (16.2)

Gross benefits paid (52.0) (42.1)

Plan amendments 48.1 —

Net projected benefit obligation at end of year $ 857.6 $ 1,135.5

The actuarial gain in 2022 was primarily attributable to a higher discount rate compared with the prior year.

The Company’s change in plan assets, funded status and amounts recognized on the Company’s consolidated balance sheets are

as follows:

years ended December 31

(in millions) 2022 2021

Fair value of plan assets at beginning of year $ 1,200.3 $ 1,037.9

Actual return on plan assets, net (171.4) 121.7

Employer contributions 90.2 82.8

Gross benefits paid (52.0) (42.1)

Fair value of plan assets at end of year $ 1,067.1 $ 1,200.3

December 31

(in millions) 2022 2021

unded status of the plan at end of year $ 209.5 $ 64.8

Accrued benefit credit $ 209.5 $ 64.8

Annual Report ♦ Page 35