Page 143 - Martin Marietta - 2023 Proxy Statement

P. 143

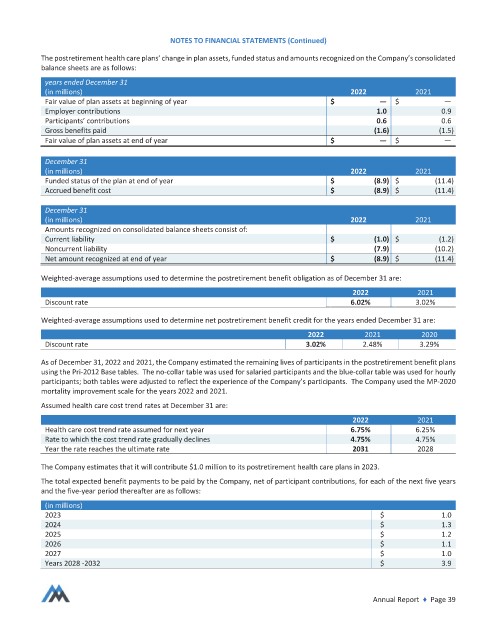

NOTES TO FINANCIAL STATEMENTS (Continued)

The postretirement health care plans’ change in plan assets, funded status and amounts recognized on the Company’s consolidated

balance sheets are as follows:

years ended December 31

(in millions) 2022 2021

Fair value of plan assets at beginning of year $ — $ —

Employer contributions 1.0 0.9

Participants’ contributions 0.6 0.6

Gross benefits paid (1.6) (1.5)

Fair value of plan assets at end of year $ — $ —

December 31

(in millions) 2022 2021

Funded status of the plan at end of year $ (8.9) $ (11.4)

Accrued benefit cost $ (8.9) $ (11.4)

December 31

(in millions) 2022 2021

Amounts recognized on consolidated balance sheets consist of:

Current liability $ (1.0) $ (1.2)

Noncurrent liability (7.9) (10.2)

Net amount recognized at end of year $ (8.9) $ (11.4)

Weighted‐average assumptions used to determine the postretirement benefit obligation as of December 31 are:

2022 2021

Discount rate 6.02% 3.02%

Weighted‐average assumptions used to determine net postretirement benefit credit for the years ended December 31 are:

2022 2021 2020

Discount rate 3.02% 2.48% 3.29%

As of December 31, 2022 and 2021, the Company estimated the remaining lives of participants in the postretirement benefit plans

using the Pri‐2012 Base tables. The no‐collar table was used for salaried participants and the blue‐collar table was used for hourly

participants; both tables were adjusted to reflect the experience of the Company’s participants. The Company used the MP‐2020

mortality improvement scale for the years 2022 and 2021.

Assumed health care cost trend rates at December 31 are:

2022 2021

Health care cost trend rate assumed for next year 6.75% 6.25%

Rate to which the cost trend rate gradually declines 4.75% 4.75%

Year the rate reaches the ultimate rate 2031 2028

The Company estimates that it will contribute $1.0 million to its postretirement health care plans in 2023.

The total expected benefit payments to be paid by the Company, net of participant contributions, for each of the next five years

and the five‐year period thereafter are as follows:

(in millions)

2023 $ 1.0

2024 $ 1.3

2025 $ 1.2

2026 $ 1.1

2027 $ 1.0

Years 2028 ‐2032 $ 3.9

Annual Report ♦ Page 39