Page 134 - Martin Marietta - 2023 Proxy Statement

P. 134

NOTES TO FINANCIAL STATEMENTS (Continued)

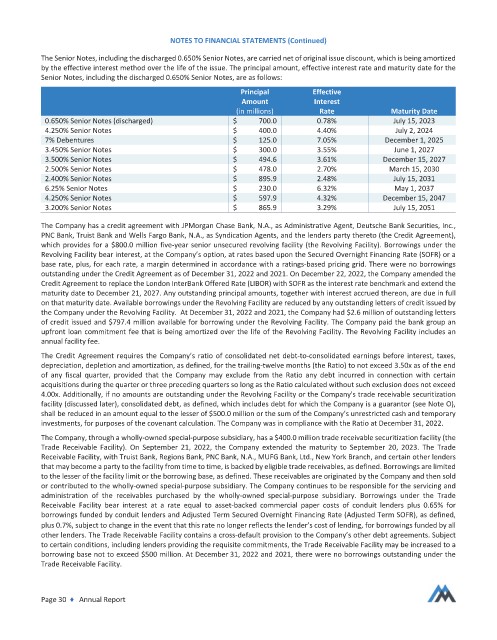

The Senior Notes, including the discharged 0.650% Senior Notes, are carried net of original issue discount, which is being amortized

by the effective interest method over the life of the issue. The principal amount, effective interest rate and maturity date for the

Senior Notes, including the discharged 0.650% Senior Notes, are as follows:

Principal Effective

Amount Interest

(in millions) Rate Maturity Date

0.650% Senior Notes (discharged) $ 700.0 0.78% July 15, 2023

4.250% Senior Notes $ 400.0 4.40% July 2, 2024

7% Debentures $ 125.0 7.05% December 1, 2025

3.450% Senior Notes $ 300.0 3.55% June 1, 2027

3.500% Senior Notes $ 494.6 3.61% December 15, 2027

2.500% Senior Notes $ 478.0 2.70% March 15, 2030

2.400% Senior Notes $ 895.9 2.48% July 15, 2031

6.25% Senior Notes $ 230.0 6.32% May 1, 2037

4.250% Senior Notes $ 597.9 4.32% December 15, 2047

3.200% Senior Notes $ 865.9 3.29% July 15, 2051

The Company has a credit agreement with JPMorgan Chase Bank, N.A., as Administrative Agent, Deutsche Bank Securities, Inc.,

PNC Bank, Truist Bank and Wells Fargo Bank, N.A., as Syndication Agents, and the lenders party thereto (the Credit Agreement),

which provides for a $800.0 million five‐year senior unsecured revolving facility (the Revolving Facility). Borrowings under the

Revolving Facility bear interest, at the Company’s option, at rates based upon the Secured Overnight Financing Rate (SOFR) or a

base rate, plus, for each rate, a margin determined in accordance with a ratings‐based pricing grid. There were no borrowings

outstanding under the Credit Agreement as of December 31, 2022 and 2021. On December 22, 2022, the Company amended the

Credit Agreement to replace the London InterBank Offered Rate (LIBOR) with SOFR as the interest rate benchmark and extend the

maturity date to December 21, 2027. Any outstanding principal amounts, together with interest accrued thereon, are due in full

on that maturity date. Available borrowings under the Revolving Facility are reduced by any outstanding letters of credit issued by

the Company under the Revolving Facility. At December 31, 2022 and 2021, the Company had $2.6 million of outstanding letters

of credit issued and $797.4 million available for borrowing under the Revolving Facility. The Company paid the bank group an

upfront loan commitment fee that is being amortized over the life of the Revolving Facility. The Revolving Facility includes an

annual facilityfee.

The Credit Agreement requires the Company’s ratio of consolidated net debt‐to‐consolidated earnings before interest, taxes,

depreciation, depletion and amortization, as defined, for the trailing‐twelve months (the Ratio) to not exceed 3.50x as of the end

of any fiscal quarter, provided that the Company may exclude from the Ratio any debt incurred in connection with certain

acquisitions during the quarter or three preceding quarters so long as the Ratio calculated without such exclusion does not exceed

4.00x. Additionally, if no amounts are outstanding under the Revolving Facility or the Company's trade receivable securitization

facility (discussed later), consolidated debt, as defined, which includes debt for which the Company is a guarantor (see Note O),

shall be reduced in an amount equal to the lesser of $500.0 million or the sum of the Company’s unrestricted cash and temporary

investments, for purposes of the covenant calculation. The Company was in compliance with the Ratio at December 31, 2022.

The Company, through a wholly‐owned special‐purpose subsidiary, has a $400.0 million trade receivable securitization facility (the

Trade Receivable Facility). On September 21, 2022, the Company extended the maturity to September 20, 2023. The Trade

Receivable Facility, with Truist Bank, Regions Bank, PNC Bank, N.A., MUFG Bank, Ltd., New York Branch, and certain other lenders

that may become a party to the facilityfrom time to time, is backed by eligible trade receivables, as defined. Borrowings are limited

to the lesser of the facility limit or the borrowing base, as defined. These receivables are originated by the Company and then sold

or contributed to the wholly‐owned special‐purpose subsidiary. The Company continues to be responsible for the servicing and

administration of the receivables purchased by the wholly‐owned special‐purpose subsidiary. Borrowings under the Trade

Receivable Facility bear interest at a rate equal to asset‐backed commercial paper costs of conduit lenders plus 0.65% for

borrowings funded by conduit lenders and Adjusted Term Secured Overnight Financing Rate (Adjusted Term SOFR), as defined,

plus 0.7%, subject to change in the event that this rate no longer reflects the lender’s cost of lending, for borrowings funded by all

other lenders. The Trade Receivable Facility contains a cross‐default provision to the Company’s other debt agreements. Subject

to certain conditions, including lenders providing the requisite commitments, the Trade Receivable Facility may be increased to a

borrowing base not to exceed $500 million. At December 31, 2022 and 2021, there were no borrowings outstanding under the

Trade Receivable Facility.

Page 30 ♦ Annual Report