Page 49 - Martin Marietta - 2023 Proxy Statement

P. 49

/ LETTER FROM COMMITTEE CHAIR

Despite notable year-over-year inflation and our 2022 divestitures, Martin Marietta had a record year, achieving our 11 th

consecutive year of growth in products and services revenues, gross profit and adjusted EBITDA. These record financial

results are a testament to Mr. Nye’s leadership, tenured experience, understanding of the cyclical nature of our business,

our team’s disciplined execution of SOAR, and unyielding focus on what we can control – including multi-year, and

industry-leading, world-class safety incident rates. We also made great progress on our Environmental, Social and

Governance (ESG) commitments and strategies. Among others, these commitments included safety, environmental

stewardship, diversity and inclusion, resilience, and employee relations.

Importantly and foundationally, the company returned to expanding aggregates margins in the fourth quarter of 2022,

underscored by an all-time quarterly record of aggregates pricing growth, which positions our company long-term to

continue delivering record years – which is anticipated in our 2023 guidance.

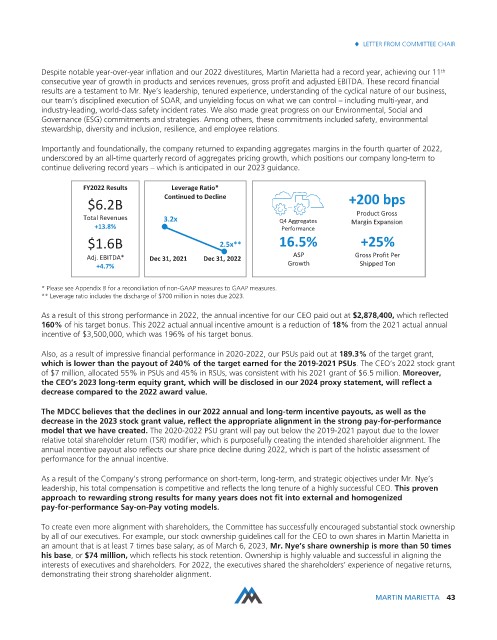

FY2022 Results Leverage Ratio*

Continued to Decline +200 bps

$6.2B

Product Gross

Total Revenues 3.2x Q4 Aggregates Margin Expansion

+13.8% Performance

$1.6B 2.5x** 16.5% +25%

Adj. EBITDA* Dec 31, 2021 Dec 31, 2022 ASP Gross Profit Per

+4.7% Growth Shipped Ton

* Please see Appendix B for a reconciliation of non-GAAP measures to GAAP measures.

** Leverage ratio includes the discharge of $700 million in notes due 2023.

As a result of this strong performance in 2022, the annual incentive for our CEO paid out at $2,878,400, which reflected

160% of his target bonus. This 2022 actual annual incentive amount is a reduction of 18% from the 2021 actual annual

incentive of $3,500,000, which was 196% of his target bonus.

Also, as a result of impressive financial performance in 2020-2022, our PSUs paid out at 189.3% of the target grant,

which is lower than the payout of 240% of the target earned for the 2019-2021 PSUs. The CEO’s 2022 stock grant

of $7 million, allocated 55% in PSUs and 45% in RSUs, was consistent with his 2021 grant of $6.5 million. Moreover,

the CEO’s 2023 long-term equity grant, which will be disclosed in our 2024 proxy statement, will reflect a

decrease compared to the 2022 award value.

The MDCC believes that the declines in our 2022 annual and long-term incentive payouts, as well as the

decrease in the 2023 stock grant value, reflect the appropriate alignment in the strong pay-for-performance

model that we have created. The 2020-2022 PSU grant will pay out below the 2019-2021 payout due to the lower

relative total shareholder return (TSR) modifier, which is purposefully creating the intended shareholder alignment. The

annual incentive payout also reflects our share price decline during 2022, which is part of the holistic assessment of

performance for the annual incentive.

As a result of the Company’s strong performance on short-term, long-term, and strategic objectives under Mr. Nye’s

leadership, his total compensation is competitive and reflects the long tenure of a highly successful CEO. This proven

approach to rewarding strong results for many years does not fit into external and homogenized

pay-for-performance Say-on-Pay voting models.

To create even more alignment with shareholders, the Committee has successfully encouraged substantial stock ownership

by all of our executives. For example, our stock ownership guidelines call for the CEO to own shares in Martin Marietta in

an amount that is at least 7 times base salary; as of March 6, 2023, Mr. Nye’s share ownership is more than 50 times

his base,or $74 million, which reflects his stock retention. Ownership is highly valuable and successful in aligning the

interests of executives and shareholders. For 2022, the executives shared the shareholders’ experience of negative returns,

demonstrating their strong shareholder alignment.

MARTIN MARIETTA 43