Page 76 - Martin Marietta - 2021 Proxy Statement

P. 76

PENSION BENEFITS / EXECUTIVE COMPENSATION

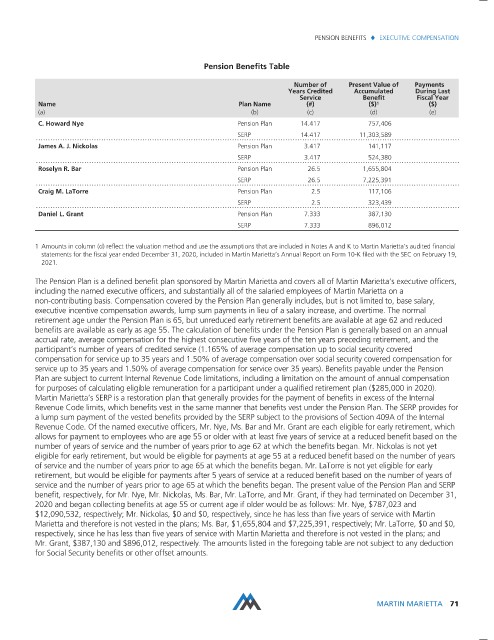

Pension Benefits Table

Number of Present Value of Payments

Years Credited Accumulated During Last

Service Benefit Fiscal Year

Name Plan Name (#) ($) 1 ($)

(a) (b) (c) (d) (e)

C. Howard Nye Pension Plan 14.417 757,406

SERP 14.417 11,303,589

James A. J. Nickolas Pension Plan 3.417 141,117

SERP 3.417 524,380

Roselyn R. Bar Pension Plan 26.5 1,655,804

SERP 26.5 7,225,391

Craig M. LaTorre Pension Plan 2.5 117,106

SERP 2.5 323,439

Daniel L. Grant Pension Plan 7.333 387,130

SERP 7.333 896,012

1 Amounts in column (d) reflect the valuation method and use the assumptions that are included in Notes A and K to Martin Marietta’s audited financial

statements for the fiscal year ended December 31, 2020, included in Martin Marietta’s Annual Report on Form 10-K filed with the SEC on February 19,

2021.

The Pension Plan is a defined benefit plan sponsored by Martin Marietta and covers all of Martin Marietta’s executive officers,

including the named executive officers, and substantially all of the salaried employees of Martin Marietta on a

non-contributing basis. Compensation covered by the Pension Plan generally includes, but is not limited to, base salary,

executive incentive compensation awards, lump sum payments in lieu of a salary increase, and overtime. The normal

retirement age under the Pension Plan is 65, but unreduced early retirement benefits are available at age 62 and reduced

benefits are available as early as age 55. The calculation of benefits under the Pension Plan is generally based on an annual

accrual rate, average compensation for the highest consecutive five years of the ten years preceding retirement, and the

participant’s number of years of credited service (1.165% of average compensation up to social security covered

compensation for service up to 35 years and 1.50% of average compensation over social security covered compensation for

service up to 35 years and 1.50% of average compensation for service over 35 years). Benefits payable under the Pension

Plan are subject to current Internal Revenue Code limitations, including a limitation on the amount of annual compensation

for purposes of calculating eligible remuneration for a participant under a qualified retirement plan ($285,000 in 2020).

Martin Marietta’s SERP is a restoration plan that generally provides for the payment of benefits in excess of the Internal

Revenue Code limits, which benefits vest in the same manner that benefits vest under the Pension Plan. The SERP provides for

a lump sum payment of the vested benefits provided by the SERP subject to the provisions of Section 409A of the Internal

Revenue Code. Of the named executive officers, Mr. Nye, Ms. Bar and Mr. Grant are each eligible for early retirement, which

allows for payment to employees who are age 55 or older with at least five years of service at a reduced benefit based on the

number of years of service and the number of years prior to age 62 at which the benefits began. Mr. Nickolas is not yet

eligible for early retirement, but would be eligible for payments at age 55 at a reduced benefit based on the number of years

of service and the number of years prior to age 65 at which the benefits began. Mr. LaTorre is not yet eligible for early

retirement, but would be eligible for payments after 5 years of service at a reduced benefit based on the number of years of

service and the number of years prior to age 65 at which the benefits began. The present value of the Pension Plan and SERP

benefit, respectively, for Mr. Nye, Mr. Nickolas, Ms. Bar, Mr. LaTorre, and Mr. Grant, if they had terminated on December 31,

2020 and began collecting benefits at age 55 or current age if older would be as follows: Mr. Nye, $787,023 and

$12,090,532, respectively; Mr. Nickolas, $0 and $0, respectively, since he has less than five years of service with Martin

Marietta and therefore is not vested in the plans; Ms. Bar, $1,655,804 and $7,225,391, respectively; Mr. LaTorre, $0 and $0,

respectively, since he has less than five years of service with Martin Marietta and therefore is not vested in the plans; and

Mr. Grant, $387,130 and $896,012, respectively. The amounts listed in the foregoing table are not subject to any deduction

for Social Security benefits or other offset amounts.

MARTIN MARIETTA 71