Page 38 - 2019 Annual Report

P. 38

NOTES TO FINANCIAL STATEMENTS (continued)

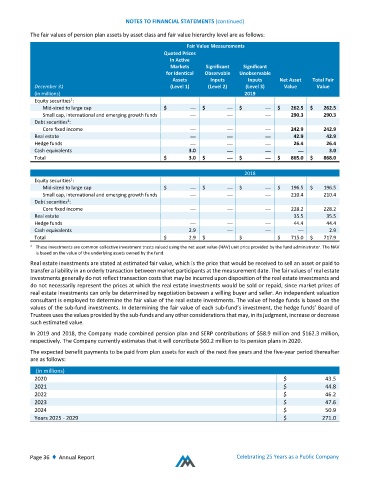

The fair values of pension plan assets by asset class and fair value hierarchy level are as follows:

Fair Value Measurements

Quoted Prices

in Active

Markets Significant Significant

for Identical Observable Unobservable

Assets Inputs Inputs Net Asset Total Fair

December 31 (Level 1) (Level 2) (Level 3) Value Value

(in millions) 2019

Equity securities :

1

Mid‐sized to large cap $ — $ — $ — $ 262.5 $ 262.5

Small cap, international and emerging growth funds — — — 290.3 290.3

Debt securities :

1

Core fixed income — — — 242.9 242.9

Real estate — — — 42.9 42.9

Hedge funds — — — 26.4 26.4

Cash equivalents 3.0 — — — 3.0

Total $ 3.0 $ — $ — $ 865.0 $ 868.0

2018

Equity securities :

1

Mid‐sized to large cap $ — $ — $ — $ 196.5 $ 196.5

Small cap, international and emerging growth funds — — — 210.4 210.4

Debt securities :

1

Core fixed income — — — 228.2 228.2

Real estate — — — 35.5 35.5

Hedge funds — — — 44.4 44.4

Cash equivalents 2.9 — — — 2.9

Total $ 2.9 $ — $ — $ 715.0 $ 717.9

1 These investments are common collective investment trusts valued using the net asset value (NAV) unit price provided by the fund administrator. The NAV

is based on the value of the underlying assets owned by the fund.

Real estate investments are stated at estimated fair value, which is the price that would be received to sell an asset or paid to

transfer a liability in an orderly transaction between market participants at the measurement date. The fair values of real estate

investments generally do not reflect transaction costs that may be incurred upon disposition of the real estate investments and

do not necessarily represent the prices at which the real estate investments would be sold or repaid, since market prices of

real estate investments can only be determined by negotiation between a willing buyer and seller. An independent valuation

consultant is employed to determine the fair value of the real estate investments. The value of hedge funds is based on the

values of the sub‐fund investments. In determining the fair value of each sub‐fund’s investment, the hedge funds’ Board of

Trustees uses the values provided by the sub‐funds and any other considerations that may, in its judgment, increase or decrease

such estimated value.

In 2019 and 2018, the Company made combined pension plan and SERP contributions of $58.9 million and $162.3 million,

respectively. The Company currently estimates that it will contribute $60.2 million to its pension plans in 2020.

The expected benefit payments to be paid from plan assets for each of the next five years and the five‐year period thereafter

are as follows:

(in millions)

2020 $ 43.5

2021 $ 44.8

2022 $ 46.2

2023 $ 47.6

2024 $ 50.9

Years 2025 ‐ 2029 $ 271.0

Page 36 ♦ Annual Report Celebrating 25 Years as a Public Company