Page 46 - Martin Marietta - 2021 Proxy Statement

P. 46

/ SUMMARY OF OUR COMPENSATION CONSIDERATIONS

In 2020, we completed our latest five-year strategic planning process, or Strategic Operating Analysis and Review

(SOAR), as previously scheduled before the COVID-19 pandemic began. The SOAR process, supplemented by our annual

plan, has guided us since 2010 as we have grown the business in an intentional, contemplative, and disciplined manner.

SOAR 2025 sets ambitious yet achievable targets for future growth and value creation.

Our impressive performance since 2010 reflects our resiliency, disciplined management, and the power of the SOAR

process:

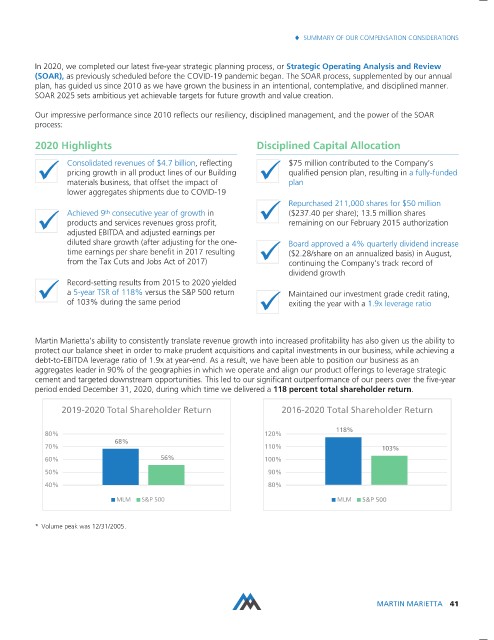

2020 Highlights Disciplined Capital Allocation

Consolidated revenues of $4.7 billion, reflecting $75 million contributed to the Company’s

pricing growth in all product lines of our Building qualified pension plan, resulting in a fully-funded

materials business, that offset the impact of plan

lower aggregates shipments due to COVID-19

Repurchased 211,000 shares for $50 million

Achieved 9 consecutive year of growth in ($237.40 per share); 13.5 million shares

th

products and services revenues gross profit, remaining on our February 2015 authorization

adjusted EBITDA and adjusted earnings per

diluted share growth (after adjusting for the one- Board approved a 4% quarterly dividend increase

time earnings per share benefit in 2017 resulting ($2.28/share on an annualized basis) in August,

from the Tax Cuts and Jobs Act of 2017) continuing the Company’s track record of

dividend growth

Record-setting results from 2015 to 2020 yielded

a 5-year TSR of 118% versus the S&P 500 return Maintained our investment grade credit rating,

of 103% during the same period exiting the year with a 1.9x leverage ratio

Martin Marietta’s ability to consistently translate revenue growth into increased profitability has also given us the ability to

protect our balance sheet in order to make prudent acquisitions and capital investments in our business, while achieving a

debt-to-EBITDA leverage ratio of 1.9x at year-end. As a result, we have been able to position our business as an

aggregates leader in 90% of the geographies in which we operate and align our product offerings to leverage strategic

cement and targeted downstream opportunities. This led to our significant outperformance of our peers over the five-year

period ended December 31, 2020, during which time we delivered a 118 percent total shareholder return.

2019-2020 Total Shareholder Return 2016-2020 Total Shareholder Return

118%

80% 120%

68%

70% 110% 103%

60% 56% 100%

50% 90%

40% 80%

MLM S&P 500 MLM S&P 500

* Volume peak was 12/31/2005.

MARTIN MARIETTA 41