Page 144 - Martin Marietta - 2025 Proxy Statement

P. 144

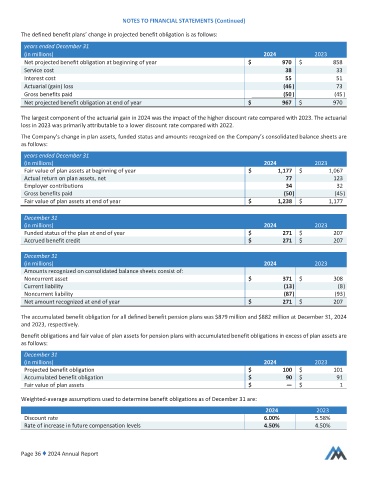

NOTES TO FINANCIAL STATEMENTS (Continued)

Thedefined benefitplans’change inprojected benefitobligation isas follows:

years ended December 31

(in millions) 2024 2023

Netprojected benefitobligationat beginning of year $ 970 $ 858

Servicecost 38 33

Interest cost 55 51

Actuarial(gain) loss (46) 73

Grossbenefitspaid (50) (45)

Netprojected benefitobligationatend of year $ 967 $ 970

Thelargest componentof the actuarialgain in2024 wasthe impact of thehigherdiscount rate compared with 2023. Theactuarial

loss in2023 wasprimarily attributable to alower discount rate compared with 2022.

The Company’schange inplanassets, fundedstatusand amounts recognizedonthe Company’sconsolidated balancesheetsare

as follows:

years ended December 31

(in millions) 2024 2023

Fair valueof planassetsat beginning of year $ 1,177 $ 1,067

Actual return on plan assets,net 77 123

Employer contributions 34 32

Grossbenefitspaid (50) (45)

Fair valueof planassets at endofyear $ 1,238 $ 1,177

December 31

(in millions) 2024 2023

Fundedstatusof the plan at endof year $ 271 $ 207

Accruedbenefit credit $ 271 $ 207

December 31

(in millions) 2024 2023

Amounts recognizedonconsolidatedbalance sheets consistof:

Noncurrent asset $ 371 $ 308

Current liability (13) (8)

Noncurrent liability (87) (93)

Netamount recognized at endofyear $ 271 $ 207

Theaccumulatedbenefit obligation for alldefined benefitpension plans was $879 millionand $882 millionat December31, 2024

and 2023, respectively.

Benefitobligations and fairvalue of plan assets forpension plans withaccumulated benefitobligations in excess of plan assets are

as follows:

December 31

(in millions) 2024 2023

Projectedbenefit obligation $ 100 $ 101

Accumulatedbenefit obligation $ 90 $ 91

Fair valueof planassets $ — $ 1

Weighted-average assumptionsusedtodetermine benefitobligations as of December 31 are:

2024 2023

scount rate 6.00% 5.58%

Rate of increase in future compensation levels 4.50% 4.50%

age36 ♦ 2024 Annual Report