Page 170 - Martin Marietta - 2024 Proxy Statement

P. 170

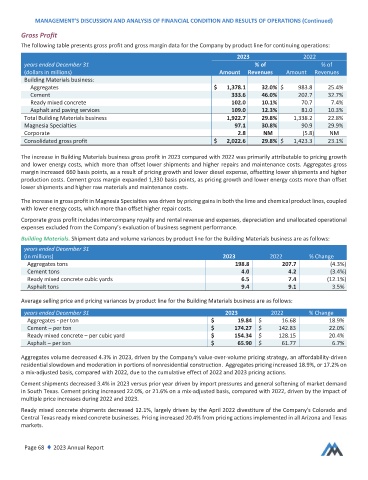

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (Continued)

Gross Profit

The following table presents gross profit and gross margin data for the Company by product line for continuing operations:

2023 2022

years ended December 31 %of %of

(dollars in millions) Amount Revenues Amount Revenues

Building Materials business:

Aggregates $ 1,378.1 32.0% $ 983.8 25.4%

Cement 333.6 46.0% 202.7 32.7%

Ready mixed concrete 102.0 10.1% 70.7 7.4%

Asphalt and paving services 109.0 12.3% 81.0 10.3%

Total Building Materials business 1,922.7 29.8% 1,338.2 22.8%

Magnesia Specialties 97.1 30.8% 90.9 29.9%

Corporate 2.8 NM (5.8) NM

Consolidated gross profit $ 2,022.6 29.8% $ 1,423.3 23.1%

The increase in Building Materials business gross profit in 2023 compared with 2022 was primarily attributable to pricing growth

and lower energy costs, which more than offset lower shipments and higher repairs and maintenance costs. Aggregates gross

margin increased 660 basis points, as a result of pricing growth and lower diesel expense, offsetting lower shipments and higher

production costs.Cement gross margin expanded 1,330 basis points, as pricing growth and lower energy costs more than offset

lower shipments and higher raw materials and maintenance costs.

The increase in gross profit in Magnesia Specialties was driven by pricing gains in both the lime and chemical product lines, coupled

with lower energy costs,which more than offset higher repair costs.

Corporate gross profit includes intercompany royalty and rental revenue and expenses, depreciation and unallocated operational

expenses excluded from the Company’s evaluation of business segment performance.

Building Materials. Shipment data and volume variances by product line for the Building Materials business are as follows:

years ended December 31

(in millions) 2023 2022 % Change

Aggregates tons 198.8 207.7 (4.3%)

Cement tons 4.0 4.2 (3.4%)

Ready mixed concrete cubic yards 6.5 7.4 (12.1%)

Asphalt tons 9.4 9.1 3.5%

Average selling price and pricing variances by product line for the Building Materials business are as follows:

years ended December 31 2023 2022 % Change

Aggregates ‐ per ton $ 19.84 $ 16.68 18.9%

Cement – per ton $ 174.27 $ 142.83 22.0%

Ready mixed concrete – per cubic yard $ 154.34 $ 128.15 20.4%

Asphalt – per ton $ 65.90 $ 61.77 6.7%

Aggregates volume decreased 4.3% in 2023, driven by the Company's value‐over‐volume pricing strategy, an affordability‐driven

residential slowdown and moderation in portions of nonresidential construction. Aggregates pricing increased 18.9%, or 17.2% on

a mix‐adjusted basis, compared with 2022, due to the cumulative effect of 2022 and 2023 pricing actions.

Cement shipments decreased 3.4% in 2023 versus prior year driven by import pressures and general softening of market demand

in South Texas.Cement pricing increased 22.0%, or 21.6% on a mix‐adjusted basis, compared with 2022, driven by the impact of

multiple price increases during 2022 and 2023.

Ready mixed concrete shipments decreased 12.1%, largely driven by the April 2022 divestiture of the Company's Colorado and

Central Texas ready mixed concrete businesses. Pricing increased 20.4% from pricing actions implemented in all Arizona and Texas

markets.

Page 68 ♦ 2023 Annual Report