Page 179 - Martin Marietta - 2023 Proxy Statement

P. 179

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (Continued)

Management’s selection of the discount rate is based on an analysis that estimates the current rate of return for high‐quality,

fixed‐income investments with maturities matching the payment of pension benefits that could be purchased to settle the

obligations. The Company selected a hypothetical portfolio of Moody’s Aa bonds, with maturities that match the benefit

obligations, to determine the discount rate. At December 31, 2022, the Company selected a discount rate assumption of 5.88%,

a 265‐basis‐point increase compared with the December 31, 2021 assumption. Of the four key assumptions, the discount rate

is generally the most volatile and sensitive estimate. Accordingly, a change in this assumption has the most significant impact

on the annual pension expense and the projected benefit obligation.

Management’s selection of the rate of increase in future compensation levels, which reflects cost of living adjustments and

merit and promotion increases, is generally based on the Company’s historical increases in pensionable earnings, while giving

consideration to anyfuture expectations. A higher rate of increase results in higher pension expense and a higher projected

benefit obligation. The assumed long‐term rate of increase is 4.50%.

Management’s selection of the expected long‐term rate of return on pension fund assets is based on a building‐block approach,

whereby the components are weighted based on the allocation of pension plan assets. Based on the currently projected returns

on these assets and related expenses, the Company selected an expected return on assets of 6.75%, the same as the prior‐year

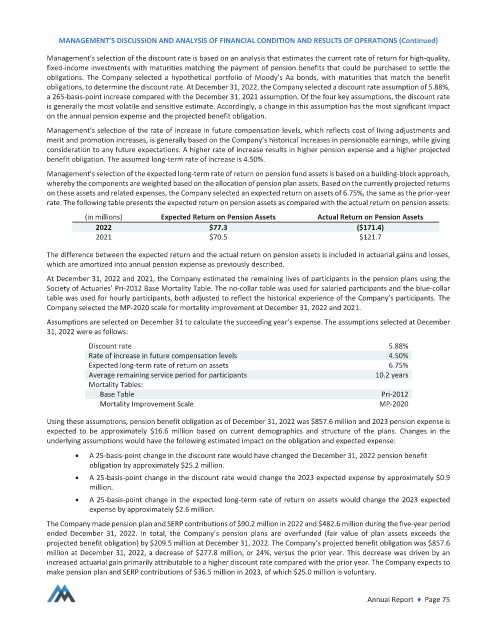

rate. The following table presents the expected return on pension assets as compared with the actual return on pension assets:

(in millions) Expected Return on Pension Assets Actual Return on Pension Assets

2022 $77.3 ($171.4)

2021 $70.5 $121.7

The difference between the expected return and the actual return on pension assets is included in actuarial gains and losses,

which are amortized into annual pension expense as previously described.

At December 31, 2022 and 2021, the Company estimated the remaining lives of participants in the pension plans using the

Society of Actuaries’ Pri‐2012 Base Mortality Table. The no‐collar table was used for salaried participants and the blue‐collar

table was used for hourly participants, both adjusted to reflect the historical experience of the Company’s participants. The

Company selected the MP‐2020 scale for mortality improvement at December 31, 2022 and 2021.

Assumptions are selected on December 31 to calculate the succeeding year’s expense. The assumptions selected at December

31, 2022 were as follows:

Discount rate 5.88%

Rate of increase in future compensation levels 4.50%

Expected long‐term rate of return on assets 6.75%

Average remaining service period for participants 10.2 years

Mortality Tables:

Base Table Pri‐2012

Mortality Improvement Scale MP‐2020

Using these assumptions, pension benefit obligation as of December 31, 2022 was $857.6 million and 2023 pension expense is

expected to be approximately $16.6 million based on current demographics and structure of the plans. Changes in the

underlying assumptions would have the following estimated impact on the obligation and expected expense:

A 25‐basis‐point change in the discount rate would have changed the December 31, 2022 pension benefit

obligation by approximately $25.2 million.

A 25‐basis‐point change in the discount rate would change the 2023 expected expense by approximately $0.9

million.

A 25‐basis‐point change in the expected long‐term rate of return on assets would change the 2023 expected

expense by approximately $2.6 million.

The Company made pension plan and SERP contributions of $90.2 million in 2022 and $482.6 million during the five‐year period

ended December 31, 2022. In total, the Company’s pension plans are overfunded (fair value of plan assets exceeds the

projected benefit obligation) by $209.5 million at December 31, 2022. The Company’s projected benefit obligation was $857.6

million at December 31, 2022, a decrease of $277.8 million, or 24%, versus the prior year. This decrease was driven by an

increased actuarial gain primarily attributable to a higher discount rate compared with the prior year. The Company expects to

make pension plan and SERP contributions of $36.5 million in 2023, of which $25.0 million is voluntary.

Annual Report ♦ Page 75