Page 172 - Martin Marietta - 2023 Proxy Statement

P. 172

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS (Continued)

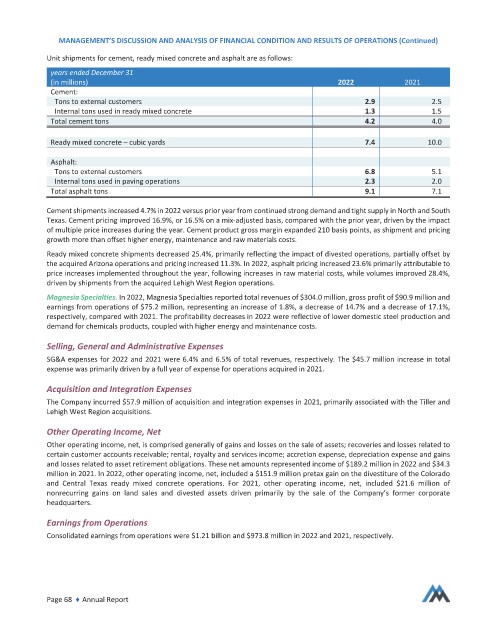

Unit shipments for cement, ready mixed concrete and asphalt are as follows:

years ended December 31

(in millions) 2022 2021

ement:

ons to external customers 2.9 2.5

Internal tons used in ready mixed concrete 1.3 1.5

Total cement tons 4.2 4.0

Ready mixed concrete – cubic yards 7.4 10.0

Asphalt:

ons to external customers 6.8 5.1

Internal tons used in paving operations 2.3 2.0

Total asphalt tons 9.1 7.1

Cement shipments increased 4.7% in 2022 versus prior year from continued strong demand and tight supply in North and South

Texas. Cement pricing improved 16.9%, or 16.5% on a mix‐adjusted basis, compared with the prior year, driven by the impact

of multiple price increases during the year. Cement product gross margin expanded 210 basis points, as shipment and pricing

growth more than offset higher energy, maintenance and raw materials costs.

Ready mixed concrete shipments decreased 25.4%, primarily reflecting the impact of divested operations, partially offset by

the acquired Arizona operations and pricing increased 11.3%. In 2022, asphalt pricing increased 23.6% primarily attributable to

price increases implemented throughout the year, following increases in raw material costs, while volumes improved 28.4%,

driven by shipments from the acquired Lehigh West Region operations.

Magnesia Specialties. In 2022, Magnesia Specialties reported total revenues of $304.0 million, gross profit of $90.9 million and

earnings from operations of $75.2 million, representing an increase of 1.8%, a decrease of 14.7% and a decrease of 17.1%,

respectively, compared with 2021. The profitability decreases in 2022 were reflective of lower domestic steel production and

demand for chemicals products, coupled with higher energy and maintenance costs.

Selling, General and Administrative Expenses

G&A expenses for 2022 and 2021 were 6.4% and 6.5% of total revenues, respectively. The $45.7 million increase in total

expense was primarily driven by a full year of expense for operations acquired in 2021.

Acquisition and Integration Expenses

The Company incurred $57.9 million of acquisition and integration expenses in 2021, primarily associated with the Tiller and

Lehigh West Region acquisitions.

Other Operating Income, Net

Other operating income, net, is comprised generally of gains and losses on the sale of assets; recoveries and losses related to

certain customer accounts receivable; rental, royalty and services income; accretion expense, depreciation expense and gains

and losses related to asset retirement obligations. These net amounts represented income of $189.2 million in 2022 and $34.3

million in 2021. In 2022, other operating income, net, included a $151.9 million pretax gain on the divestiture of the Colorado

and Central Texas ready mixed concrete operations. For 2021, other operating income, net, included $21.6 million of

nonrecurring gains on land sales and divested assets driven primarily by the sale of the Company’s former corporate

headquarters.

Earnings from Operations

Consolidated earnings from operations were $1.21 billion and $973.8 million in 2022 and 2021, respectively.

Page 68 ♦ Annual Report